If you've ever held a perpetual futures position and found that your balance slowly decreased even when the price didn't move against you, you've experienced funding rates. Funding rates are one of the most misunderstood mechanics in crypto trading — and one of the most exploitable by traders who understand them.

This guide explains what funding rates are, why they exist, how to read them on Solana perp DEXs like Drift Protocol, and how sophisticated traders use funding rates to generate consistent income.

What Are Funding Rates?

Perpetual futures are derivatives that let you speculate on price without an expiration date. Unlike traditional futures that must settle at expiry, perps can be held indefinitely. To keep the perp price anchored to the spot price, exchanges use a mechanism called funding rates.

The basic idea:

- If there are more longs than shorts (perp price > spot), longs pay shorts

- If there are more shorts than longs (perp price < spot), shorts pay longs

- Payments happen every 1-8 hours depending on the protocol

This creates an economic incentive: when longs outnumber shorts and funding is positive, new shorts are incentivized to open positions (they'll get paid). This pressure brings the perp price back toward spot.

Why Funding Rates Exist

Without funding rates, a perpetual future could diverge from spot price indefinitely. If everyone is bullish and goes long, the perp price would trade at a permanent premium to spot — which would be economically absurd.

Funding rates solve this by making the "crowded side" of the trade pay the uncrowded side. The more longs outnumber shorts, the higher the funding rate, the more expensive it becomes to stay long.

How Funding Rates Are Calculated

The exact formula varies by protocol, but the general calculation is:

Funding Rate = Clamp(Premium Index, -Cap, +Cap)

Where:

- Premium Index = (Mark Price - Index Price) / Index Price

- Mark Price = the current perp price

- Index Price = the spot price from oracle feeds

- Cap = maximum funding rate (e.g., ±0.05% per 8 hours)

Practical example:

- SOL spot price: $150

- SOL perp mark price: $151.50

- Premium = ($151.50 - $150) / $150 = 1% = 0.01

- If the cap is 0.05% per hour, the 0.01 premium translates to a positive funding rate

Positive funding → longs pay shorts

Negative funding → shorts pay longs

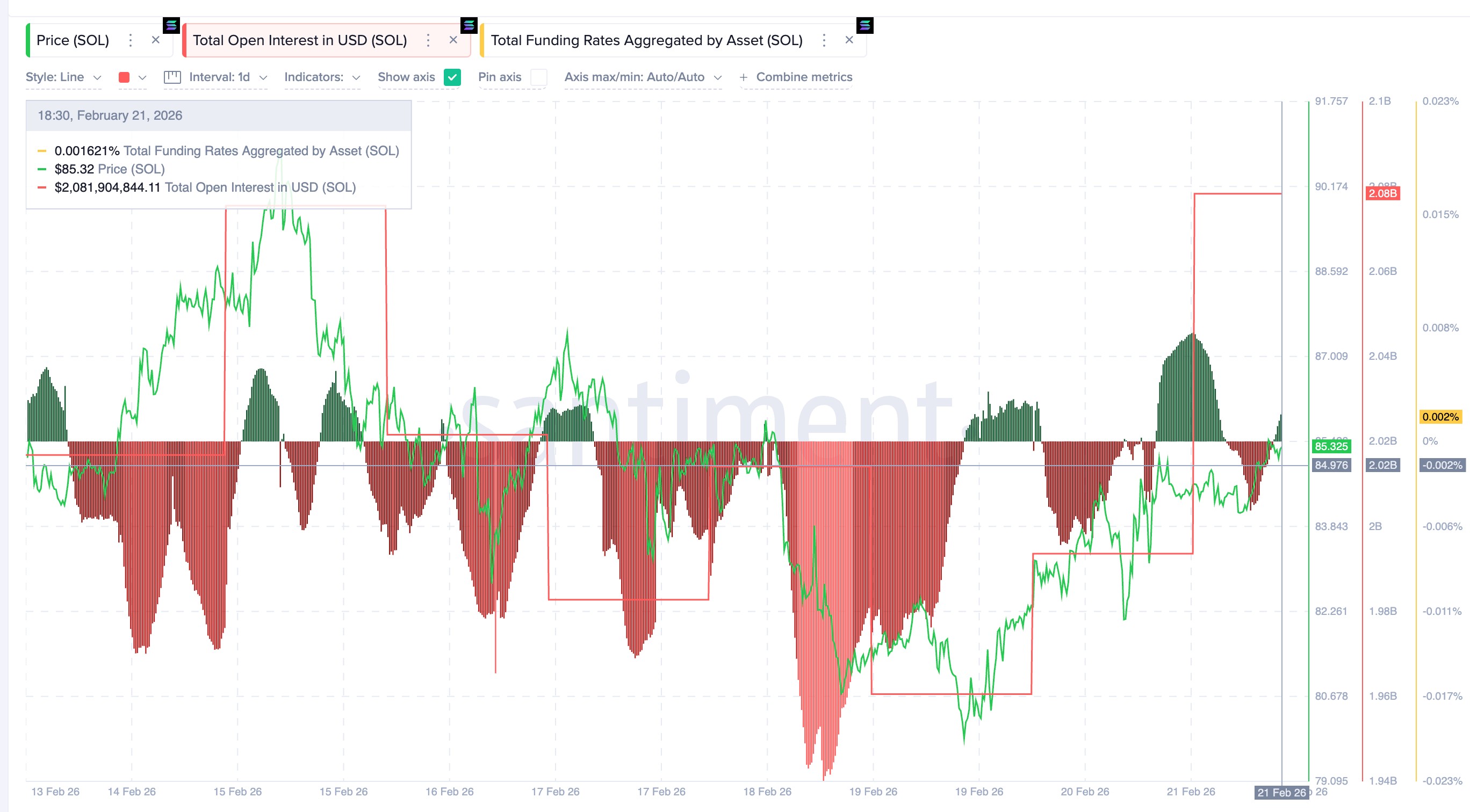

Drift Protocol is Solana's largest perpetual DEX by volume. Here's how to read funding rates:

- Go to app.drift.trade

- Select any perpetual market (e.g., SOL-PERP)

- In the market info panel, you'll see:

- Current Funding Rate: Shown as % per period (e.g., "0.012% / hour")

- Funding Countdown: Time until the next funding payment

- Mark Price vs Oracle Price: How far the perp is trading from spot

If funding is +0.02% per hour:

- You're paying 0.02% per hour if long

- You're receiving 0.02% per hour if short

- Over 24 hours: 0.48% per day paid/received

- Over a week: ~3.36% — significant on a leveraged position

Annualized Funding Rate Context

To understand whether a funding rate is high or low, annualize it:

Annual Rate = Hourly Rate × 8,760 hours

| Hourly Rate | Daily | Annual |

|---|

| 0.001% | 0.024% | 8.76% |

| 0.005% | 0.12% | 43.8% |

| 0.010% | 0.24% | 87.6% |

| 0.050% | 1.2% | 438% |

During bull markets, funding rates on popular tokens (SOL, BTC, memecoins) can reach 100-500%+ annualized. This is both a cost for those holding longs and an opportunity for those willing to run the short side.

This is the strategy professional traders use to earn funding rate income without directional risk:

The setup:

- Buy the asset spot (e.g., buy 10 SOL)

- Open a short perpetual position of equal size (short 10 SOL-PERP)

- Your net exposure to SOL price is zero (long spot + short perp = neutral)

- You collect the funding rate payment from longs without directional risk

Example:

- SOL price: $150

- You buy 10 SOL for $1,500

- You open a 10 SOL short on Drift with $1,500 collateral

- Funding rate: +0.015% per hour (longs paying shorts)

- You receive 0.015% × $1,500 = $0.225 per hour

- Daily income: $5.40

- Annual run rate: ~$1,971 on $3,000 deployed (~65.7% APY)

When funding flips negative (shorts paying longs), you reverse: sell spot, close short, open long to collect from shorts.

Risks of the carry trade

- Liquidation risk: Your short position on Drift needs collateral. A sharp price spike can liquidate it before you can add margin. Use conservative leverage (2-3x max)

- Execution risk: Getting in and out of both legs simultaneously is tricky. Price moves between trades

- Funding rate reversal: Funding can flip from positive to negative, turning your income stream into a cost

- Counterparty and smart contract risk: Protocol-level risk exists on both the spot and perp side

- Basis risk: Slight differences between the oracle price and real market price can create minor losses